SMM, February 21:

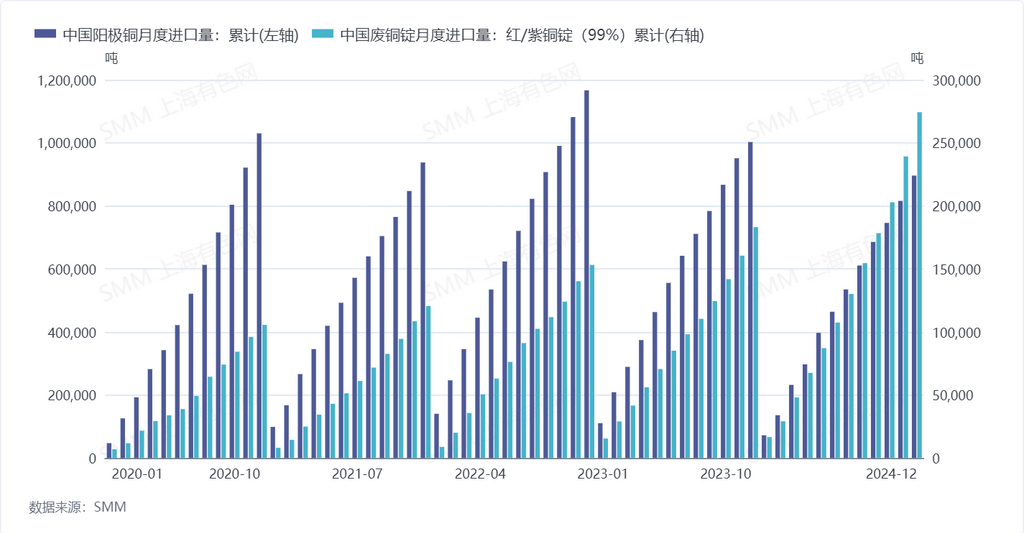

According to data from the General Administration of Customs, China's copper anode import volume totaled 896,000 mt in January-December 2024, down 10.62% YoY; China's copper scrap ingot (red/purple copper ingot) import volume totaled 274,200 mt in January-December 2024, up 49.77% YoY.

In terms of import sources, China's copper anode imports mainly came from Africa, South America, and Asia. In 2024, Zambia accounted for 47.20% of the import volume; the DRC accounted for 14.07%; Chile accounted for 12.18%; and South Africa accounted for 7.06%.

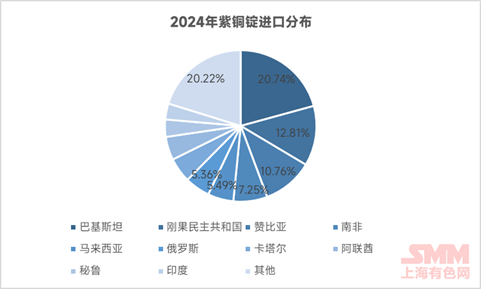

China's copper scrap ingot (red/purple copper ingot) imports mainly came from Asia and Africa. In 2024, Pakistan accounted for 20.74% of the import volume; the DRC accounted for 12.81%; Zambia accounted for 10.76%; and South Africa accounted for 7.25%.

Reviewing the import data over the past five years, from 2020 to 2024, China's copper anode import volumes were 1.03 million mt, 937,700 mt, 1.1664 million mt, 1.0025 million mt, and 896,000 mt, respectively. Affected by the shift to shortage in copper concentrate raw materials and the expansion of overseas copper smelting and refining capacity, the supply of imported copper anodes has significantly declined in the past two years. In contrast, China's copper scrap ingot (red/purple copper ingot) imports grew rapidly from 2020 to 2024, with volumes of 105,700 mt, 120,600 mt, 153,200 mt, 183,100 mt, and 274,200 mt, respectively.

The differing trends in import volumes of the two materials in recent years also reflect changes in China's copper raw material market. While China's copper cathode capacity has expanded annually, its reliance on copper concentrate imports remains high. With frequent mining incidents at the end of 2023, the global copper concentrate balance shifted to a shortage in 2024, leading to a sharp decline in TC prices. Facing losses and tight raw material supply, smelters significantly increased their demand for copper scrap and copper anode raw materials. However, the limited supply of overseas copper anodes made from ore has greatly driven the growth in imports of copper scrap and copper scrap ingots.

In 2025, with a major mine's crude refining project in the DRC expected to commence operations, China's copper anode imports are anticipated to rebound. However, this essentially represents a transfer of copper content, and thus, domestic smelters' demand for copper scrap raw materials is expected to continue expanding.